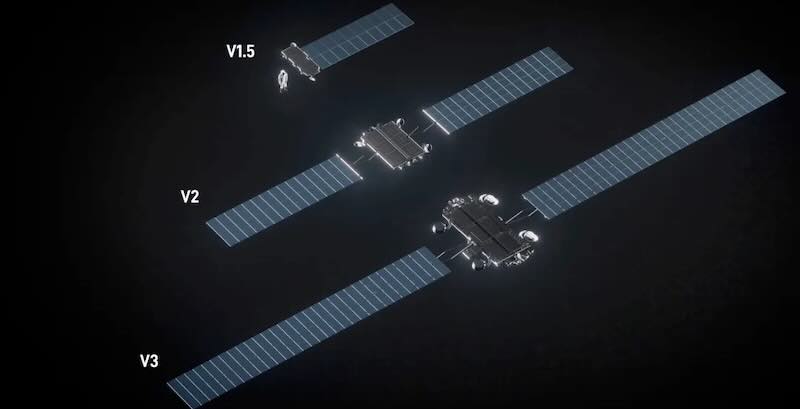

GlobalStar [NASDAQ: GSAT] 2025 Annual Report. Dr. Paul E. Jacobs, GlobalStar's CEO: “We advanced our strategy across every dimension of the business: from global infrastructure expansion to product innovation and growing commercial adoption across government, enterprise, and industrial markets. We expanded our addressable markets and validated technologies that position us at the center of next-generation satellite and private wireless connectivity. Throughout the year, we have made significant progress with our satellite and ground station partners and are now poised to deploy not only the satellites to replenish our existing constellation but also extend our reach with our third-generation system."

✅ Nvidia hiring for orbital data center system architect, as the space compute market grows. Base salary: USD 224,000 - USD 356,500. "The role will 'drive architecture for orbital data center systems considering everything from the chip out to the satellite and connectivity between satellites, and work on building a roadmap for ✅ Nvidia products in space.'" [DCD: 4 Mar 2026]

Spacex has acquired X.AI Corp, maker of the Grok large language model and owner of the X social network. [The Batch: 13 Feb 2026]

Pengana Capital Group (PCG.AX) has doubled the valuation of Elon Musk’s SpaceX to USD 800 billion (AUD 1.1 trillion), with its prized stake expected to generate big returns for the money manager as the rocket company prepares for a blockbuster initial public offering (IPO) in the coming months. The Sydney-based firm previously valued the hotly anticipated IPO at USD 400 billion, but upped its valuation following a secondary share sale in Dec 2025. [Pengana: 11 Mar 2026]

⏯️ Elon Musk is merging SpaceX and xAI firms, with plans for space-based AI data centres. Musk says solar powered and space-based data centres are the only way to meet AI’s burgeoning energy demands. [More about the merger: WSJ 5 Feb 2026] [xAI: 12 Feb 2026]

To achieve this, SpaceX wants to launch a constellation of 1 million satellites that will orbit Earth and harness the sun to power AI data centers, according to an 18 Sep 2025 filing at the Federal Communications Commission (FCC) and GN Docket No. 25-302. [⏯️ WAI]

The filing was made by:

This filing has been accepted by the FCC for filing: 30 Sep 2025

Companies (in addition to Spacex) with credible proposals for orbital data centers include:

World Economic Forum Davos 2026 Interviews

⏯️ TED Lecture: Philip Johnston [Reuters/ChatGPT]

"Blue Origin has been working on technology for AI data centers in space, building on Jeff Bezos' prediction that "giant gigawatt data centers" in orbit could beat the cost of their Earth-bound peers within 10 to 20 years by tapping uninterrupted solar power and radiating heat directly into space."

Starcloud has already offered a glimpse of that future: its 60KG Starcloud-1 satellite, launched on a Spacex Falcon 9 rocket on 2 Nov 2025, carries an ✅ Nvidia H100 - the most powerful AI chip ever placed in orbit - and is training and running ✅ Google’s open‑source Google’s open large language model, Gemma, as a proof of concept.

Progress & Developments:

This project marks the first time a high-powered AI model has been operated in space. [Starcloud White Paper, Sep 2024]

The company ultimately envisions a modular “hypercluster” of satellites providing about five gigawatts of computing power, comparable to several hyperscale data centers combined. [Reuters/ChatGPT] [White Paper: Aug 2024]

Spacex orbital data centers

Spacex orbital data centers

"Space data center startup Starcloud has revealed plans to launch ✅ Amazon Web Services (AWS) on-prem/Edge offering, ✅ AWS Outposts, in space, as well as its long-term goal of an 88,000-satellite constellation. [GitHub White Paper: Sep 2024 ]

Co-founder and CEO of Starcloud, Philip Johnston, revealed the partnership with ✅ AWS in a LinkedIn post on February 9. "I am excited to share that Starcloud will be the first to launch the ✅ Amazon Web Services (AWS) Outpost hardware to space on our second satellite launching in October this year, further enabling high-performance computing in space!"

AWS Outposts are rack and server-level offerings from ✅ AWS, enabling customers to bring AWS capabilities to their own data center or Edge location. Launched in 2018, the cloud giant unveiled a new generation in April 2025 that could support AWS' seventh-generation x86-powered ✅ Amazon EC2 instances, beginning with the C7i compute-optimized instances, C7i general-purpose instances, and R7i memory-optimized instances." About instance types.

Spacex is seeking Federal Communications Commission approval for a satellite constellation of unprecedented scale intended to function as an orbital data center.

Orbital Data Centers may be maintained by NASA's Integrated System for Autonomous and Adaptive Caretaking (ISAAC), which is a project aimed at developing autonomous robots to maintain space stations. The ISAAC project, based at NASA’s Ames Research Center and Johnson Space Center, developed technology for autonomous caretaking of spacecraft, primarily during uncrewed mission phases. ISAAC aimed to integrate autonomous intra-vehicular robots with vehicle infrastructure.

As of March 2026, SpaceX has acquired AI startup xAI, creating a combined entity valued at approximately USD 1.25 trillion to USD 1.8 trillion. This merged entity plans to pursue an IPO later in 2026, aiming to develop space-based AI data centers using Starlink. The move combines profitable rocket tech with high-cash-need AI. [KraneShares: 11 Jan 2026]

ChatGPT offers the following comments on some issues involved in a space-based data center:

In summary, ChatGPT outlines the following issues - in descending order of difficulty:

"SpaceX has developed a novel Space Situational Awareness (SSA) system, called Stargaze, that significantly enhances the safety and sustainability of satellite operations in low Earth orbit (LEO), and its screening data will be made available to the broader satellite operator community free of charge in the coming weeks.

Practices such as leaving rocket bodies in LEO, operators maneuvering their satellites without sharing trajectory predictions or coordinating with other active satellites, and countries conducting anti-satellite tests—have heightened the risk of collision, necessitating improvements in space-traffic coordination. Conventional methods typically observe objects only a limited number of times per day, causing large uncertainties in orbital predictions, further compounded by volatile space weather." [Spacex]

Stargaze delivers a several-order-of-magnitude increase in detection capability compared to conventional ground-based systems. Stargaze uses data collected from nearly 30,000 star trackers, each of which makes continuous observations of nearby objects, resulting in approximately 30 million transits detected daily across the fleet." Reuters 13 Feb 2026

Elon Musk has discussed the step beyond data centers orbiting Earth is even larger computers in deep space. And furthermore, Musk says the best way to achieve that is to build a city on the moon to manufacture space computers and hurl them into the solar system using a big maglev train. [TechCrunch, Spacex: 12 Feb 2026]

Vision: Moonbase Alpha: LEV FLOAT Lunar Transport

Vision: Moonbase Alpha: LEV FLOAT Lunar Transport

In an X.com post on 8 Feb 2026, Elon Musk explained the focus on the moon as a higher priority than Mars:

"...Spacex has already shifted focus to building a self-growing city on the Moon, as we can potentially achieve that in less than 10 years, whereas Mars would take 20+ years. The mission of Spacex remains the same: extend consciousness and life as we know it to the stars.

It is only possible to travel to Mars when the planets align every 26 months (six month trip time), whereas we can launch to the moon every 10 days (2 day trip time). This means we can iterate much faster to complete a Moon city than a Mars city.

That said, Spacex will also strive to build a Mars city and begin doing so in about 5 to 7 years, but the overriding priority is securing the future of civilisation and the Moon is faster."

⏯️ Elon Musk prioritises Moonbase Alpha [17 Feb 2026]

"SpaceX proposes to conduct ⏯️ Starship/Super Heavy launch operations from the ⏯️ Boca Chica Launch Site in Cameron County, Texas. SpaceX must apply for and obtain an experimental permit(s) and/or a vehicle operator license from the FAA Office of Commercial Space Transportation to operate the ⏯️ Starship/Super Heavy launch vehicle ... SpaceX is developing a new rocket, ⏯️ Starship/Super Heavy, with the goal of traveling to Mars." FAA 13 Feb 2026

⏯️ Spacex Starship vs NASA SLS

"The space race between US billionaires is heating up, with Elon Musk's SpaceX planning to build a lunar base and Jeff Bezos pushing Blue Origin's ambitions as both companies aim to return humans to the moon ahead of a planned mission by China in 2030." Reuters 13 Feb 2026

DataCenters.com lists 9,049 data centers globally of which 270 are in Australia. That requires a lot of electricity - representing potentially related opportunities for investment in power generation.

✅ Amazon acquires George Washington University's Virginia data center [Reuters: 2 Mar 2026]

This is an investor's view of investment opportunities in AI technical infrastructure, prepared with data from ClaudeAI and Blackridge [6 Feb 2026]. [Report]

| Data Center | Mkt Cap | Location | Sites |

|---|---|---|---|

| 365 Data Centers [Not listed] | Private | Connecticut | |

| ✅ Alphabet [NASDAQ:GOOG/L] | ~USD 1.9 trillion | ||

| ✅ Amazon [NASDAQ:AMZN] | ~USD 1 trillion | Amazon | |

| Broadcom [NASDAQ:AVGO] | ~USD 1.59 - USD 1.62 trillion | Oracle | |

| Cologix [NASDAQ:COGIX] | Colorado | 29 | |

| Core Scientific [NASDAQ:CORZ] | Colorado | ||

| CyrusOne [NASDAQ:CONE: KKR and GIP] | CAD 92.4bn+3.2m | Texas | 25 |

| Databank [Not listed] | Texas | 23 | |

| Digital Realty Trust Inc [NYSE:DLR] | USD 60.5 bn | Texas | 115 |

| Equinix Inc [NASDAQ: EQIX] | USD 90.8 bn | Redwood | >200 |

| Flexential [NASDAQ:FLEX] | USD 24.3 bn | North Carolina | 40 |

| IBM [NYSE:IBM] | USD 112 bn | 11 | |

| Iron Mountain [NYSE: IRM] | USD 31.3 bn | Massachusetts | 25 |

| Microsoft [NASDAQ:MSFT] | ~USD 2.9 trillion | Microsoft Azure | |

| ✅ Nvidia [NASDAQ:NVDA] | ~USD 4.0-5.1 trillion | Nvidia | |

| Oracle [NYSE:ORCL] | ~USD 434 billion | Oracle | |

| QTS Technology Centers [Private] | Private | Kansas | 40 |

| Vantage Data Centers | Private | Colorado | 25 |

✅ Meta jumped 5.1% after Reuters reported that the social media platform plans to shrink its workforce by 20% or more to offset costly artificial-intelligence infrastructure bets and prepare for greater efficiency brought about by AI-assisted workers. [Reuters 13 Mar 2026]

✅ Meta data center

✅ Meta is rapidly expanding its global data center infrastructure to support massive AI workloads, transitioning toward gigawatt-plus, "super-intelligence" facilities. Key 2025-2026 projects include massive sites in Louisiana, Ohio, Indiana, and Texas, utilizing 100% renewable energy. These AI-optimized, sustainable, and locally-supported data centers drive Meta’s "Compute" division, focusing on large-language models and future AI, with the company spending over $600 billion in the US by 2028. [Meta 13 Mar 2026]

Several Australian companies are launching portable, containerised data centers. These include:

Armada Edge Platform (AEP) portable data center convoy.

"WinDC aims to place data center infrastructure at power generation sites and will deploy 11MW of modular data centers designed and built by Armada and its partners across renewable energy sites in New South Wales and other locations in the National Energy Market Operator's systems, as well as in Western Australia. Armada Edge units are currently built in the United States and Europe." DCD 16 Mar 2026

Proximity to fiber optic networks: Cities like Ashburn, Silicon Valley, and Dallas are known for their interconnectivity.

Energy supply: Sustainable, renewable energy is becoming a key factor in investment decisions.

Local regulatory environment: Different states have varying regulations on data privacy and energy usage that could impact long-term operational viability.

Future growth plans: Many of the major players are expanding or making significant upgrades to their existing campuses.

TIER 1 - Mission Critical (Highest AI Value):

TIER 2 - Highly Important:

TIER 3 - Supporting Infrastructure:

Vertiv (VRT) - Liquid cooling & power infrastructure for AI datacenters

Eaton (ETN) - Power distribution critical as clusters scale

Coherent (COHR) - Optical transceivers (competes with Marvell)

ASML (ASML) - ⏯️ EUV extreme ultra violet photo lithography monopoly (enables everything, though not US-listed):

✅ Nvidia (Nvidia) - The elephant in the room for GPUs. Nvidia has kicked off the next generation of AI With Rubin 6 new chips, one incredible AI supercomputer. Rubin is in full production, and Rubin-based products will be available from partners in the second half of 2026. The Rubin platform uses extreme codesign across the 6 chips — the Nvidia Vera CPU, Nvidia Rubin GPU, Nvidia 6 Switch, Nvidia ConnectX®-9 SuperNIC, Nvidia BlueField®-4 DPU and Nvidia Spectrum™-6 Ethernet Switch — to slash training time and inference token costs. [Nvidia press release: 5 Jan 2026]

AMD (AMD) - MI300X competing with ✅ Nvidia.

Super Micro (SMCI) - AI server integration

Dell/HPE - AI infrastructure deployment

And also:

✅ We are investors in these companies

Sidebar: ⏯️ About chip production [ASML] by Veritasium

Stargate AI Data Center in Abilene, Texas is the first and flagship site of a USD 500 billion national AI infrastructure initiative announced in Jan 2025. Located on a 1,000–1,100 acre tract known as the Lancium Clean Campus (also called the Crusoe Abilene Campus), the facility is under construction and nearing completion.

Objectives: Stargate will secure American leadership in AI, create hundreds of thousands of American jobs, and generate massive economic benefit for the entire world. This project will not only support the re-industrialization of the United States but also provide a strategic capability to protect the national security of America and its allies.

Capacity: The facility is designed to deliver 1.2 gigawatts (GW ❓) of power at full scale, with 200 MW❓ already deployed as of early 2025. It is powered by a combination of renewable energy and on-site natural gas generation, utilizing Lancium’s Smart Response™ technology for grid optimization and decarbonization.

❓ Note: References to MW, GW and TW in the context of data centers are electrical power capacity, not compute output.

Key Partners The data center is being developed by Crusoe Energy Systems LLC and operated in partnership with OpenAI and Oracle. The site is a cornerstone of the Stargate project. The initial equity funders in Stargate are:

SoftBank and OpenAI are the lead partners for Stargate, with SoftBank having financial responsibility and OpenAI having operational responsibility.

As part of Stargate, Oracle, Nvidia, and OpenAI will closely collaborate to build and operate this computing system. This builds on a deep collaboration between OpenAI and Nvidia going back to 2016 and a newer partnership between OpenAI and Oracle.

This project also builds on the existing OpenAI partnership with Microsoft. OpenAI will continue to increase its consumption of Azure as OpenAI continues its work with Microsoft with this additional compute to train leading models and deliver great products and services.

Lancium report on provision of clean energy for the Abilene facility. [Lancium: 18 Mar 2025] Lancium has secured USD 600 million debt financing for 1.2GW ❓ clean energy development for the Abilene project [Lancium: 18 Oct 2025]

❓ Note: References to MW, GW and TW in the context of data centers are electrical power capacity, not compute output.

Masayoshi Son, SoftBank's CEO will be the chairman.

Oracle has committed to developing 4.5 gigawatts of data center capacity for OpenAI, with this Abilene site being a major component. OpenAI signed a deal to purchase USD 300 billion in computing power from Oracle over 5 years, starting in 2027" [WSJ 10 Sep 2025].

Economic Impact: The project has created approximately 6,000 construction jobs and is projected to generate $4 billion in economic impact over the next two decades. It has boosted local spending, tax revenues, and spurred infrastructure development, including a new 1,000-unit housing project.

Expansion Plans: OpenAI and Oracle have abandoned plans to expand the facility from 1.2 GW to 2 GW due to financing challenges and shifting demand forecasts. However, ✅ Meta Platforms is evaluating a lease for the additional capacity, with Nvidia facilitating discussions and having paid a USD 150 million deposit to Crusoe to secure its interest.

Note: References to MW, GW and TW in the context of data centers are electrical power capacity, not compute output.

Challenges: The project has caused traffic disruptions, environmental concerns, and a housing crisis in Abilene due to the sudden influx of workers. Some data center buildings experienced outages in early 2026 due to winter weather affecting liquid cooling systems, though both Crusoe and Oracle report strong ongoing collaboration.

The Abilene Stargate site is a pivotal hub in the global AI infrastructure race, combining massive scale, renewable energy integration, and complex logistics, even as expansion plans have been paused. [Lancium: 18 Mar 2025]

Project Financing Problems: Some partners are reconsidering their commitment to Stargate. Oracle and OpenAI have abandoned plans to expand the Stargate AI data center after negotiations dragged over financing and OpenAI's changing needs. [Bloomberg: 7 Mar 2026]

The collapsed talks created an opening for ✅ Meta Platforms to step in and consider leasing the planned expansion site in Abilene, Texas, from developer Crusoe, with ✅ Nvidia helping facilitate Meta’s discussions.

✅ Nvidia paid a USD 150 million deposit to Crusoe and began helping court Meta as a tenant for the expansion, to ensure its products would still fill the expanded data center rather than that of rival Advanced Micro Devices Inc.

Status as at 30 Sep 2025: The site is operational with 10 buildings under construction, and two buildings are already up and running. The campus is expected to be fully completed by the end of 2026.

Status as at Mar 2026: Oracle and OpenAI have abandoned plans to expand their 1.2 GW ❓ AI data center in the Stargate project, from 1.2 GW to 2 GW ❓ due to financing negotiations and shifting infrastructure needs. The initial 1.2 GW ❓ site remains active as part of the Stargate AI project, with ✅ Meta now considering taking over the expanded capacity.

❓ Note: References to MW, GW and TW in the context of data centers are electrical power capacity, not compute output.

Wall Street Millenial [W M] is now referring to OpenAI's USD110 billion funding round as mostly fake, and refers to Stargate as a hoax. W💲M alleges that Sam Altman is not an AI expert, and has no formal education in AI. ⏯️ W💲M discusses OpenAI's funding situation. ColdFusion reports that OpenAI may start incorporating advertisements in its responses.

✅ Amazon's 1,200 acre Anthropic data center in Northern Indiana will support 500,000 ✅ AWS Trainium 2 and ✅ AWS Trainium 3 chips. This number will increase to 1 million chips by the end of 2025.

Power for the data center will be provided by Northern Indiana Public Service Co (NIPSCO). To support the energy requirements of that data center, NIPSCO Generation will build about 3 gigawatts of new generation capacity, including new gas-fired power plants and battery storage systems. [ChatGPT]

The initial cost of the Rainer data center campus and related facilities is estimated to be around USD 26 billion:

🇺🇸 ✅ Amazon plans to spend USD 12 billion on AI data centers in the Caddo and Bossier Parishes of Northern Louisiana. [CNBC 23 Feb 2026]

✅ Amazon Louisiana Data Center

"Anthropic is expanding to Australia and New Zealand. In the coming weeks, we will open an office in Sydney—our fourth office in Asia-Pacific, alongside Tokyo, Bengaluru, and Seoul. The expansion reflects strong demand from businesses in Australia and New Zealand and will help us better serve the countries’ unique AI ecosystems.

"In addition to hiring a team in Sydney, we plan to deepen our engagement with Australian institutions, as well as collaborate on projects that advance Australia’s national interests and priority sectors. Our executive team will visit Australia at the end of March to formalize some of these partnerships and meet with customers and policymakers.

"Our initial focus will be supporting our enterprise, startup, and research customers. Anthropic already works with some of Australia and New Zealand's most innovative organizations—from enterprises like Canva, Quantium, and Commonwealth Bank of Australia, to startups pioneering new AI applications across diverse fields such as AgTech, physical AI, climate tech and more.

"Australia and New Zealand rank 4th and 8th globally in Claude.ai usage, relative to population, according to our latest Economic Index. Both countries show strong use of Claude for computer and coding tasks, along with educational instruction and research, and we’ve already begun building out a local team and partnerships aligned with these trends."

🇦🇺 Anthropic's report on Australia suggests that its usage is the 4th highest of 166 countries. Report: 15 Jan 2026 Update: 10 Mar 2026

🌏 Claude says Anthropic has offices in San Francisco, Seattle, New York, and Washington D.C. Anthropic's European footprint includes offices in London, Dublin, Zurich, Paris, and Munich. In Asia-Pacific Anthropic has offices Tokyo, Bengaluru (India), and Seoul.

🇦🇺 Anthropic has announced its intention to establish an office in Sydney. Its objective is to meet local data residency requirements for government and enterprise clients, using existing local third-party infrastructure. This will be its 4th office in Asia Pacific. [Anthropic: 10 Mar 2026].

Anthropic has announced a USD 50 billion investment to develop, own, and operate its own data centers in the United States, starting in Texas and New York, in partnership with UK-based Fluidstack. Anthropic's approach is a "hybrid" model: relying on massive, existing infrastructure from ✅ AWS and ✅ Google (1M+ chips), while simultaneously building a USD 50 billion custom-operated, AI-optimized data center footprint via Fluidstack to ensure long-term, independent scaling. [Anthropic

Fluidstack is rapidly scaling its capacity to serve major clients like Meta and various AI startups.

Some of the largest data centers in USA:

✅ Amazon acquires George Washington University's Virginia data center [Reuters: 2 Mar 2026]

This is an investor's view of investment opportunities in AI technical infrastructure, prepared with ClaudeAI and Blackridge [6 Feb 2026].

| Data Center | Mkt Cap | Location | Sites |

|---|---|---|---|

| 365 Data Centers | Private | Connecticut | |

| ✅ Alphabet [GOOG/L] | ~$1.9 trillion | ||

| ✅ Amazon [AMZN] | ~$1 trillion | Amazon | |

| Broadcom [AVGO] | ~$914 trillion | Oracle | |

| Cologix | Colorado | 29 | |

| Core Scientific | Colorado | ||

| CyrusOne [CONE: KKR and GIP] | 92.4bn+3.2m CAD | Texas | 25 |

| Databank | xx bn | Texas | 23 |

| Digital Realty Trust Inc [NYSE:DLR] | 60.5 bn | Texas | 115 |

| Equinix Inc [NASDAQ: EQIX] | 90.8 bn | Redwood | >200 |

| Flexential [NASDAQ:FLEX] | 24.3 bn | North Carolina | 40 |

| IBM | 112 bn | IBM | 11 |

| Iron Mountain[NYSE: IRM] | 31.3 bn | Massachusetts | 25 |

| Microsoft [MSFT] | ~$2.9 trillion | Microsoft Azure | |

| ✅ Nvidia [NVDA] | ~$4.0-5.1 trillion | Nvidia | |

| Oracle [ORCL] | ~$434 billion | Oracle | |

| QTS Technology Centers [Private] | Private | Kansas | 40 |

| Vantage Data Centers | Private | Colorado | 25 |

Proximity to fiber optic networks: Cities like Ashburn, Silicon Valley, and Dallas are known for their interconnectivity.

Energy supply: Sustainable, renewable energy is becoming a key factor in investment decisions.

Water supply: Data centres in Sydney currently consume approximately 3.5 billion litres of drinking water annually, mostly for cooling. Sydney Water, Australia’s largest water utility, has estimated data centres’ use of Sydney’s water supply could jump to 25% by 2035. [AFR: 27 Jan 2026]

Local regulatory environment: Different states have varying regulations on data privacy and energy usage that could impact long-term operational viability.

Future growth plans: Many of the major players are expanding or making significant upgrades to their existing campuses.

TIER 1 - Mission Critical (Highest AI Value):

TIER 2 - Highly Important:

TIER 3 - Supporting Infrastructure:

Vertiv (VRT) - Liquid cooling & power infrastructure for AI datacenters

Eaton (ETN) - Power distribution critical as clusters scale

Coherent (COHR) - Optical transceivers (competes with Marvell)

ASML (ASML) - EUV extreme ultra violet photo lithography monopoly (enables everything, though not US-listed):

✅ Nvidia (NVDA) - The elephant in the room for GPUs. NvidiaGoogle: 6 new chips, one incredible AI supercomputer. Rubin is in full production, and Rubin-based products will be available from partners in the second half of 2026. The Rubin platform uses extreme codesign across the 6 chips — the Nvidia Vera CPU, Nvidia Rubin GPU, Nvidia NVLink™ 6 Switch, Nvidia ConnectX®-9 SuperNIC, Nvidia BlueField®-4 DPU and Nvidia Spectrum™-6 Ethernet Switch — to slash training time and inference token costs. [Nvidia press release: 5 Jan 2026]

AMD (AMD) - MI300X competing with ✅ Nvidia

Super Micro (SMCI) - AI server integration

Dell/HPE - AI infrastructure deployment

And also:

✅ We are investors in these companies

"✅ AWS said two UAE facilities were hit directly, while in Bahrain, a drone strike in close proximity to one of its facilities caused physical impacts to our infrastructure.

The company said the drones caused structural damage, disrupted power delivery to infrastructure, and in some cases, required fire suppression activities that resulted in additional water damage.

The firm added that it is working quickly to restore services to the affected areas, but that it could take time given the nature of the physical damage involved.

It also recommended that customers who use its services in the region back up their data and "potentially migrate workloads" to alternative AWS facilities in the rest of the world.

✅ AWS also warned that the ongoing conflict means "the broader operating environment in the Middle East remains unpredictable." [BBC: 1 Mar 2026]

Australia has 270 data centers, some of which are targetable as investments. The ASX lists 100 of those data centers, 13 of which are large cap companies.

The Data Center's latest update reports that Australia has 270 data centers [14 Mar 2026]

| Location | Number |

|---|---|

| Adelaide | 18 |

| Albury | 2 |

| Ballarat | 3 |

| Bendigo | 1 |

| Brisbane | 24 |

| Canberra | 18 |

| Christmas Island | 1 |

| Coffs Harbour | 1 |

| Darwin | 6 |

| Dubbo | 1 |

| Geraldton | 2 |

| Gold Coast | 1 |

| Grafton | 1 |

| Hobart | 5 |

| Launceston | 1 |

| Melbourne | 51 |

| Morwell | 1 |

| Moss Vale | 1 |

| Newcastle AU | 5 |

| Newman | 1 |

| Perth | 26 |

| Port Hedland | 1 |

| Sunshine Coast | 2 |

| Sydney | 91 |

| Tamworth | 1 |

| Toowoomba | 1 |

| Townsville | 2 |

| Wagga Wagga | 1 |

| Wollongong | 1 |

| Total Data Centers | 270 |

✅ NextDC Limited [ASX:NXT] has 22 data centers in Australia and others in New Zealand, Japan and Malaysia. It is planning to invest a further AUD 2.7 billion in data centers in 2026 to meet AI demand [AFR 25 Feb 2026]:

NextDC has held a series of calls and meetings with credit investors across Australia ahead of a planned four-year and seven-year AUD 500 million subordinated bond issue. [AFR 15 Mar 2026]

| Location | Data Center | Owner | Capacity ❓ |

|---|---|---|---|

| Melbourne | AirTrunk MEL1 | AirTrunk | ~276 MW |

| Sydney | AirTrunk SYD2 | AirTrunk | ~158 MW |

| Sydney | AirTrunk SYD1 | AirTrunk | ~121 MW |

| Melbourne (West Footscray) | NEXTDC M3 | ✅ NextDC | ~150 MW |

| Sydney (Artarmon) | NEXTDC S3 | ✅ NextDC | ~80 MW |

| Sydney (Eastern Creek) | DC1-DC4 | Infratil | ~100 MW+ |

| Sydney (Alexandria) | Equinix SY5 | Equinix | large multi-hall colocation (~9,000 cabinets) |

| Sydney East/West | Global Switch | Global Switch | ~70 MW+ |

| Melbourne (Tullamarine) | NEXTDC M2 | ✅ NEXTDC | ~40 MW+ |

| Melbourne (Brooklyn) | CDC BK1 | CDC | ~780 MW+ |

❓ Note: References to MW, GW and TW in the context of data centers are electrical power capacity, not compute output.

The [AFR reports: 12 Mar 2026] that "✅ Google has told the federal government that it is withholding an AUD 20 billion investment in a massive Australian artificial intelligence and data center hub because of the risk of exposing its broader operations to higher taxes. Google is assessing where to build its Asian hub, and Australia is among the leading candidates due to abundant land and sun, as solar power is likely to be used to power the data center.

"Tax was one of the key discussion points, according to a Treasury briefing prepared for Treasurer Chalmers before the meeting and released on 7 Mar 2026 in response to a freedom of information request. Google is particularly sensitive about perceptions that it is seeking special tax treatment.

"✅ Google, ✅ Amazon and ✅ Microsoft are investing billions of dollars in digital infrastructure in Australia, largely by leasing space from local data centre operators AirTrunk, ✅ NextDC and ✅ CDC Data Centres. That also includes investments in chips, connecting cables and renewable energy.

"The existing cloud data centres are much smaller than the AI and data centre hub that Google is considering building and operating in Australia.

"The proposed AI and data centre hub would be of a similar scale to the huge 1 gigawatt AI data hub in India that ✅ Google committed to in October at an estimated cost of USD 15 billion (AUD 21.5 billion) between now and 2030." [AFR 16 Mar 2026]

Google has told the Australian federal government that it is withholding a AUD 20 billion investment in a massive Australian artificial intelligence and data center hub because of the risk of exposing its broader operations to higher taxes.

Australia has been more aggressive than many jurisdictions on:

That creates uncertainty, which is often worse than high tax rates.

Data Center Water Usage: "By 2027, AI and data centre operations globally are projected to consume between 4.2 and 6.6 billion cubic metres of water annually. That’s equivalent to around 30–45% of Australia’s entire yearly water consumption. This surge has occurred in just a few years, reflecting the exponential rise of AI workloads and the infrastructure needed to power them." [Sphere Infrastructure: 10 Sep 2025]

❓ Note: References to MW, GW and TW in the context of data centers are electrical power capacity, not compute output.

Airtrunk is a hyperscale data centre specialist providing a secure and reliable solution for cloud, content and large enterprise customers to house high volumes of data and information. It is an example of strong private investment in data centers. AirTrunk was founded in 2015 by Robin Khuda and has remained privately owned for most of its life. Khuda was a founding member of ✅ NextDC. In Sep 2024, Airtrunk was acquired by funds manager Blackstone Inc and the Canada Pension Plan Investment Board for about AUD 24 billion. Because of that buyout, Airtrunk continues to operate as a privately held portfolio company. ChatGPT comments: "The landscape is oddly fascinating: real estate fused with hyperscale computing." [Blackstone's Sydney Office: Suite 5, Level 30, Governor Macquarie Tower, 1 Farrer Place, Sydney]

Airtrunk's SYD3 data center in Western Sydney. Airtrunk is no longer listed on the ASX.

CDC develops, owns and operates large scale data centers across Australia and New Zealand. It is not listed on the ASX.

CDC's SYD3 data center at Eastern Creek, Western Sydney.

Goodman Group operates data centers in Tokyo, Hong Kong and Frankfurt. It also operates data center power banks in USA (San Jose, Los Angeles), Europe (London, Amsterdam, Frankfurt, Paris, Milan, Barcelona, Madrid), Hong Kong, Japan (Tokyo, Osaka), Australia (Sydney, Melbourne) and New Zealand (Auckland). Goodman is Australia’s largest developer of industrial property, strategically located with easy access to large consumer markets in Sydney, Melbourne and Brisbane. Goodman is listed on the ASX as ASX:GMG.

Goodman's SYD-01 data center at North Sydney.

TechInvestment.com is an investor in ✅ NextDC.

✅ NextDC has 17 data centers in Australia: Sydney (7), Melbourne (5), Brisbane (3), Perth (2).

✅ NextDC will join OpenAI in Australia as an infrastructure partner.

✅ NextDC's Port Melbourne data center.